U.S. futures experienced a decline on Monday as markets across Asia showed notable gains. This shift occurred after Federal Reserve Chair Jerome Powell revealed that the Department of Justice had issued subpoenas to the central bank. The potential for a criminal indictment stemming from questions related to Powell’s testimony about a significant $2.5 billion renovation project has intensified the ongoing conflict between Powell and former President Donald Trump, who has criticized the renovations as excessive.

Asian markets reacted positively to the news. The Hang Seng index in Hong Kong surged by 1.2%, closing at 26,547.64, while the Shanghai Composite index rose by 1% to 4,163.11, following reports that Chinese authorities were preparing additional economic support measures. In contrast, U.S. futures saw declines, with the S&P 500 futures falling by 0.6%, the Dow Jones Industrial Average futures decreasing by 0.5%, and the Nasdaq composite index futures slipping by 0.9%.

Despite the turbulent backdrop, the U.S. dollar remained stable against the Japanese yen, trading at 158.02 yen. Meanwhile, South Korea’s Kospi index climbed by 0.8% to 4,624.79, and Australia’s S&P/ASX 200 gained 0.5%, closing at 8,759.40. Taiwan’s Taiex also recorded a 0.9% increase.

U.S. stock markets had reached record highs on Friday, with the S&P 500 climbing 0.6% to 6,966.28, surpassing its previous all-time high. The Dow Jones Industrial Average rose by 0.5% to 49,504.07, and the Nasdaq composite achieved a 0.8% gain, closing at 23,671.35. A mixed report from the U.S. Labor Department indicated that employers hired fewer workers than anticipated in December, although improvements in the unemployment rate suggested that the job market remains resilient.

As the situation develops, Powell’s term as chair of the Federal Reserve is set to conclude in May, with speculation that Trump may appoint a replacement soon. Trump has also attempted to dismiss Fed governor Lisa Cook, intensifying the scrutiny on the Federal Reserve’s leadership. In an interview with NBC News on Sunday, Trump claimed he was unaware of the investigation into Powell, denying that it was intended to pressure him regarding interest rates.

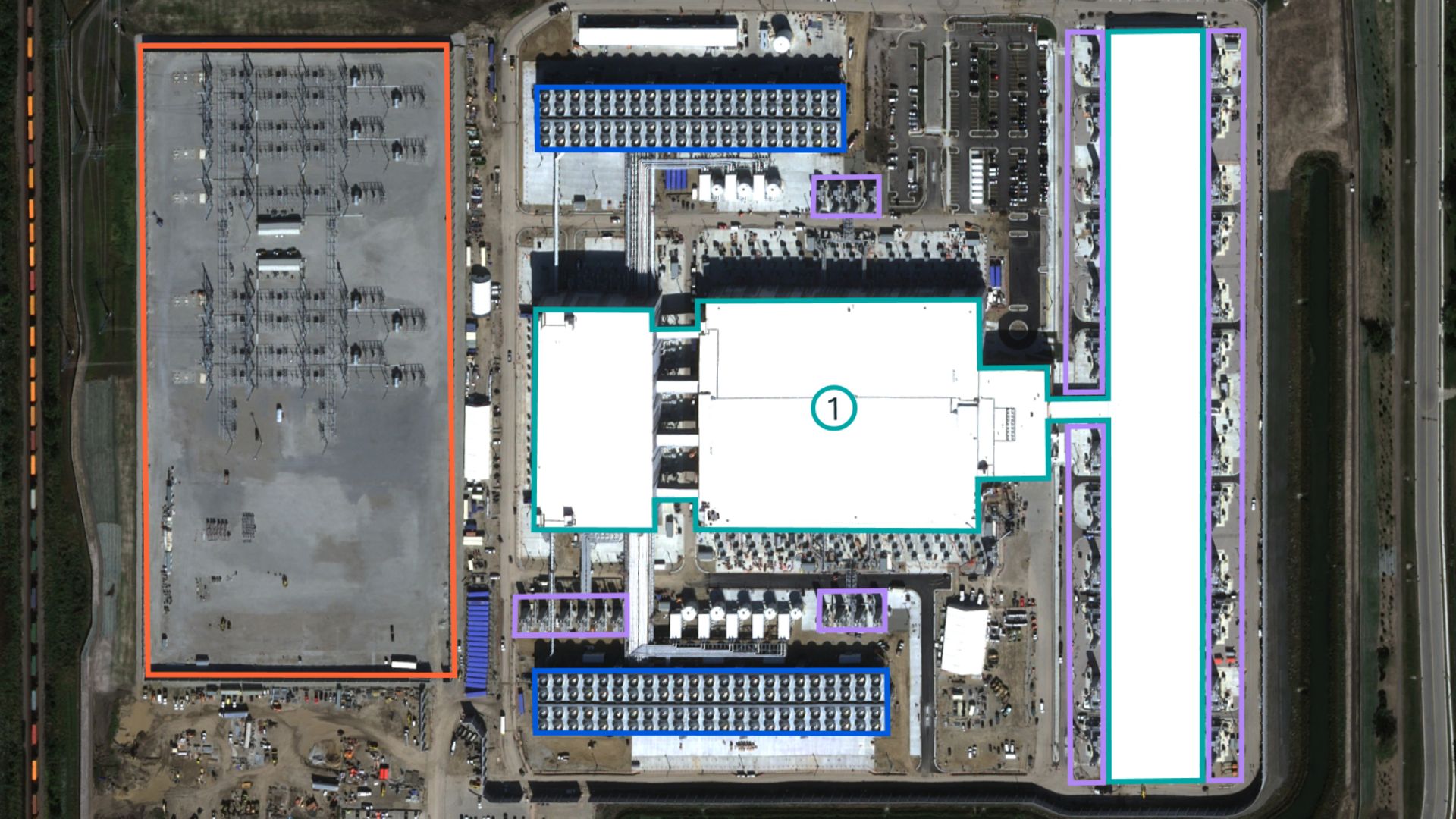

In the energy sector, the U.S. power company Vistra saw its stock soar by 10.5% after securing a 20-year agreement to supply electricity from three nuclear plants to Meta Platforms. This move is part of a broader trend among tech companies looking to electrify their data centers as they expand into artificial intelligence technologies.

Further bolstering market sentiment, homebuilders responded positively to Trump’s announcement of a plan aimed at reducing mortgage rates. He proposed purchasing $200 billion in mortgage bonds, reminiscent of previous Federal Reserve measures to lower rates. This led to significant gains among homebuilding companies: Builders FirstSource surged 12%, while Lennar, D.R. Horton, and PulteGroup saw increases of 8.9%, 7.8%, and 7.3%, respectively.

Conversely, General Motors faced challenges, announcing a projected $6 billion loss for the last quarter of 2025 due to a strategic pullback from electric vehicles. This follows an earlier $1.6 billion charge in the previous quarter, attributed to decreased demand linked to fewer tax incentives and relaxed fuel-emission regulations.

On the commodities front, the euro rose against the U.S. dollar, climbing to $1.1671 from $1.1635 late on Friday. U.S. benchmark crude oil prices increased by 8 cents to $59.20 per barrel, while Brent crude rose by 9 cents to $63.43 per barrel. Precious metals also saw price increases, with gold rising by 1.9% and silver by 6.4%. Additionally, copper prices gained 1.4%.

As the week unfolds, updates regarding U.S. inflation are expected, with a consumer inflation report due on Tuesday, followed by wholesale price data on Wednesday. These economic indicators will be closely monitored as markets respond to ongoing developments in both domestic and global contexts.