More than 23 million Americans enrolled in Affordable Care Act (ACA) plans are bracing for increased health care costs next year as federal funding for subsidies is set to expire on December 31, 2023. This potential rise in costs has prompted Democrats in Congress to withhold their votes on a government spending bill, urging Republicans to extend these critical subsidies that lower insurance costs for individuals purchasing health coverage through ACA marketplaces.

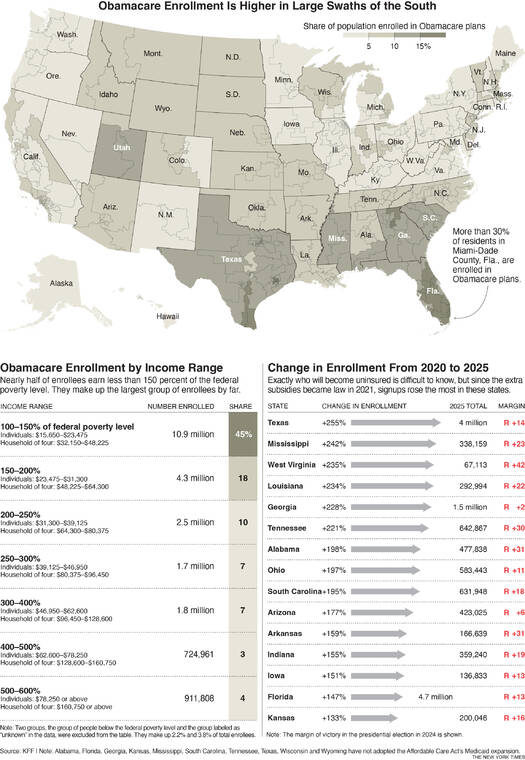

Since the introduction of additional funding in 2021, enrollment in these plans has more than doubled. The beneficiaries of these subsidies are spread across the nation, but their concentration is particularly notable in several red states. These states have opted not to expand Medicaid programs to include low-income, childless adults. In fact, approximately 57 percent of ACA enrollees reside in Republican congressional districts, highlighting a significant disparity in coverage based on state policies.

The ACA was designed to assist the poorest Americans through Medicaid and to provide subsidies for those earning slightly more. This has resulted in a unique overlap in eligibility, where individuals may qualify for Medicaid in some states but require subsidies in others. States that have not expanded Medicaid since the ACA’s encouragement in 2014 have seen a surge in low-income individuals qualifying for subsidies.

Enrollment has tripled in six predominantly Republican states—Texas, Louisiana, Mississippi, Tennessee, Georgia, and West Virginia. Notably, West Virginia and Louisiana have expanded Medicaid, which contrasts with the trends in other states. The distribution of ACA coverage is particularly pronounced in South Florida, where a high number of low-wage workers and early retirees rely on these plans.

The most affected demographic by the loss of subsidies will be those earning less than 150 percent of the federal poverty level, approximately $24,000 annually for an individual or $48,000 for a family of four. This group predominantly consists of individuals in low-paying jobs without employer-sponsored health insurance, part-time workers, and gig economy freelancers. The enhanced subsidies introduced in 2021 have allowed many in this income bracket to avoid monthly premium payments entirely, provided they choose one of the two lowest-cost plans available.

Despite the benefits, critics argue that the generous nature of these subsidies has led to instances of fraud. Should these subsidies be allowed to expire, monthly premiums for the lowest-income enrollees could rise significantly, estimated to range from $27 to $82 each month.

As Congress debates the future of these subsidies, the outcome will have profound implications for millions of Americans relying on affordable health care coverage, especially in states that have opted out of expanding Medicaid. The looming deadline for subsidy renewal has created a critical juncture for both lawmakers and enrollees as they navigate the complexities of health care affordability in the United States.