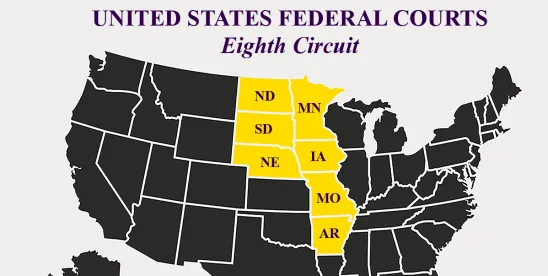

On July 25, 2025, the U.S. Court of Appeals for the Eighth Circuit upheld a ruling from the District Court affirming that the Mayo Clinic is entitled to a refund of $11.5 million in unrelated business income taxes. This decision stems from the court’s classification of the Mayo Clinic as an “educational organization” under section 170(b)(1)(A)(ii) of the Internal Revenue Code.

The court’s ruling confirms that educational organizations, such as the Mayo Clinic, can qualify for an exemption from taxes on unrelated business taxable income (UBTI), particularly related to acquisition indebtedness. The Eighth Circuit’s decision reinforces that an organization can be deemed educational even if its educational activities are not its sole focus.

Key Legal Arguments

The government’s appeal argued that education does not constitute the Mayo Clinic’s principal purpose. The government posited that merely having educational components is insufficient for qualifying as an educational organization. This argument directly challenged the District Court’s interpretation, which defined “primary” as “substantial” in the context of educational activities.

In its ruling, the Eighth Circuit sided with the District Court’s interpretation, drawing on precedent established in the Supreme Court case of Board of Governors v. Agnew. In that case, the Supreme Court determined that the term “primary” can be understood as synonymous with “essentially” or “fundamentally,” allowing for multiple substantial activities to coexist.

The court emphasized that the Mayo Clinic’s education, patient care, and research are interlinked, making it challenging to isolate a single predominant activity. By interpreting “primary” to mean “substantial,” the court aligned its decision with Treasury Regulations that recognize various types of educational organizations.

Clinical Practice vs. Educational Purpose

The government contended that the Mayo Clinic’s extensive clinical practice disqualified it from the UBTI exemption, arguing that its activities were more aligned with a commercial enterprise rather than an educational institution. The government referenced the Mayo Clinic’s nationwide hospital network and extensive patient care services, suggesting that these operations resemble a profit-driven business model.

Both the District Court and the Eighth Circuit rejected this perspective. The District Court found that while patient care is indeed a significant purpose of the organization, it is not a noneducational function at the Mayo Clinic. Evidence revealed no clinical practice that operates independent of the educational mission.

The Eighth Circuit further supported the District Court’s conclusion, noting that patient care is integrated with educational objectives, demonstrating that an organization can legitimately pursue multiple purposes simultaneously.

Final arguments from the government sought to categorize the Mayo Clinic as a hospital rather than an educational entity, asserting that hospitals do not qualify for the UBTI exemption. The Eighth Circuit dismissed this classification, affirming that the Mayo Clinic possesses attributes of both a hospital and an educational institution, thereby justifying its claim under the UBTI exemption.

Looking ahead, this ruling may have implications for how multi-purpose tax-exempt institutions are assessed regarding their educational status under section 170(b)(1)(A)(ii). While this decision may open the door for similar institutions to claim the UBTI exemption, it remains closely tied to the unique circumstances of the Mayo Clinic. Future institutions seeking similar treatment must demonstrate a comparable intertwining of educational and other activities to be eligible for the same benefits.